Uber, Stellantis, And Wayve Want To Blanket The World In Robotaxis

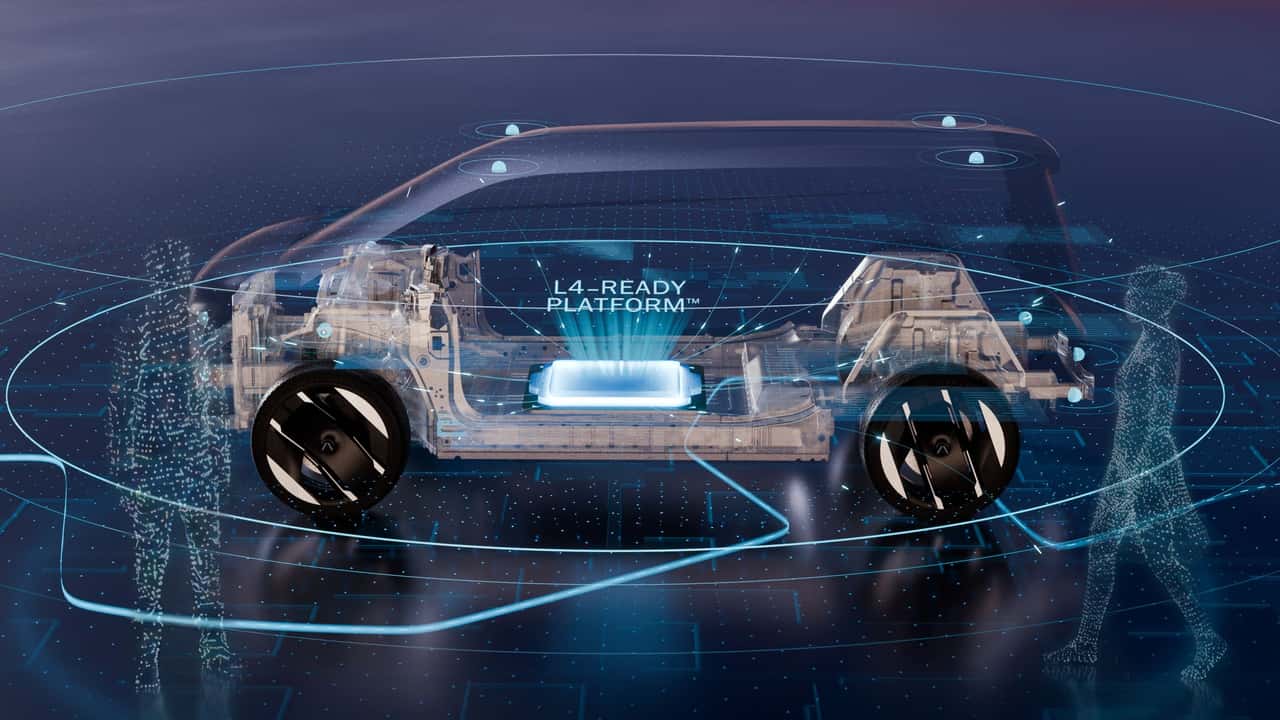

Uber is expanding its robotaxi strategy by partnering with Stellantis and UK AI firm Wayve to deploy autonomous vehicles globally.

2 comments

Sign in to join the discussion.

Sign inUber's platform play exposes the industry's unresolved tension: camera-based systems like Wayve's promise lower hardware costs, but their safety validation under ISO 26262 ASIL-D remains immature compared to lidar-redundant architectures that have logged billions of supervised miles. Stellantis brings manufacturing scale, yet integrating AV stacks across vehicle variants introduces configuration management nightmares that automotive functional safety wasn't designed to handle at software deployment speeds. The real test isn't customer adoption—it's whether regulators will approve geofenced expansions without transparent crash causation data and independent safety case reviews. Operators banking on this model should demand contractual clarity on liability allocation when the inevitable edge-case failure occurs, because Uber's asset-light structure deliberately diffuses accountability across the technical stack. Without standardized safety metrics between partners, this becomes a race to whichever jurisdiction asks the fewest questions.

Uber's AV aggregator model masks a brutal operational reality: robotaxi fleets still require human oversight, remote intervention networks, cleaning rotations, charging logistics, and 24/7 maintenance dispatch—all cost centers that erode the promised unit economics advantage over human drivers. Fleet uptime targets of 95%+ demand predictive diagnostics and rapid swap infrastructure that neither Stellantis nor Wayve has proven at commercial scale. The smartest near-term play isn't full autonomy—it's hybrid dispatch that routes low-complexity trips to AVs while keeping experienced drivers for weather, construction zones, and edge cases where human judgment remains cheaper than remote ops overhead. Total cost of ownership only improves when vehicle utilization exceeds 16 hours daily without degrading service reliability, a threshold no robotaxi operator has sustainably achieved outside controlled pilots.